Source: Deloitte: Curt Fedder United States Barb Renner United States Jagadish Upadhyaya India

Disruptive technologies are often redefining the way consumer products companies are doing business. Blockchain can potentially help them create more value, achieve operational efficiencies, and enhance customer experience.

DISRUPTIVE digital technologies, such as blockchain, artificial intelligence (AI), digital reality (DR), and cloud, are potentially ushering in a new era of productivity for consumer products companies. These technologies are not only helping spur efficient internal processes, innovation, brand growth, and profitability, but also enhancing the consumer experience. Addressing the potential of blockchain, this is the first article of a short-article series on the theme of disruptive technologies. To realize the full potential and benefits of disruptive digital technologies, consumer products companies can benefit from understanding where they are on their journey to digital maturity and how they can implement these technologies to meet their digital transformation goals.

Consumer products companies’ journey toward digital maturity

In the 2018 Annual Study of Digital Business,1 MIT Sloan Management Review and Deloitte analyzed digital maturity of various industries. The 2018 study is based on responses of 4,300 business executives across 123 countries representing 28 industries. Digital maturity is calculated based on respondents’ rating of their company on a scale of 1 to 10, with 1 being the lowest.2

In the 2018 Annual Study of Digital Business,1 MIT Sloan Management Review and Deloitte analyzed digital maturity of various industries. The 2018 study is based on responses of 4,300 business executives across 123 countries representing 28 industries. Digital maturity is calculated based on respondents’ rating of their company on a scale of 1 to 10, with 1 being the lowest.2

Interestingly, on the spectrum of digital maturity, respondents from the consumer products industry rated it as being in the mid-to-lower end of the digital-maturity spectrum in comparison to other consumer-facing industries (figure 1). As such, while the consumer products industry has been making strides in this regard through efforts such as automating manufacturing processes, introducing online shopping, and digitizing the supply chain, there appears to remain ample opportunity for continued digital transformation.

To move forward on their journey to digital maturity and harness the power of disruptive technologies,

consumer products companies will likely benefit by focusing on the following steps that can enable their success:

- Make digital systems and infrastructure a priority

- Upskill existing talent with digital skills

- Replace manual processes with digital

- Drive innovations with digital at the core

Indeed, it is likely easier for startup organizations that are more nimble to implement disruptive technologies than it is for well-established companies with greater infrastructure in place. Regardless, consumer products organizations could start by defining the business imperative for growth, identifying and structuring their data to support growth, and leverage disruptive technologies to optimize, interpret, and apply the data.

Blockchain: Potential and use cases in the consumer products industry

Blockchain is one technology that has the potential to usher in a new era of transparency for consumer products companies and consumers alike. A recent Deloitte publication, , describes in detail how blockchain works (figure 2).3

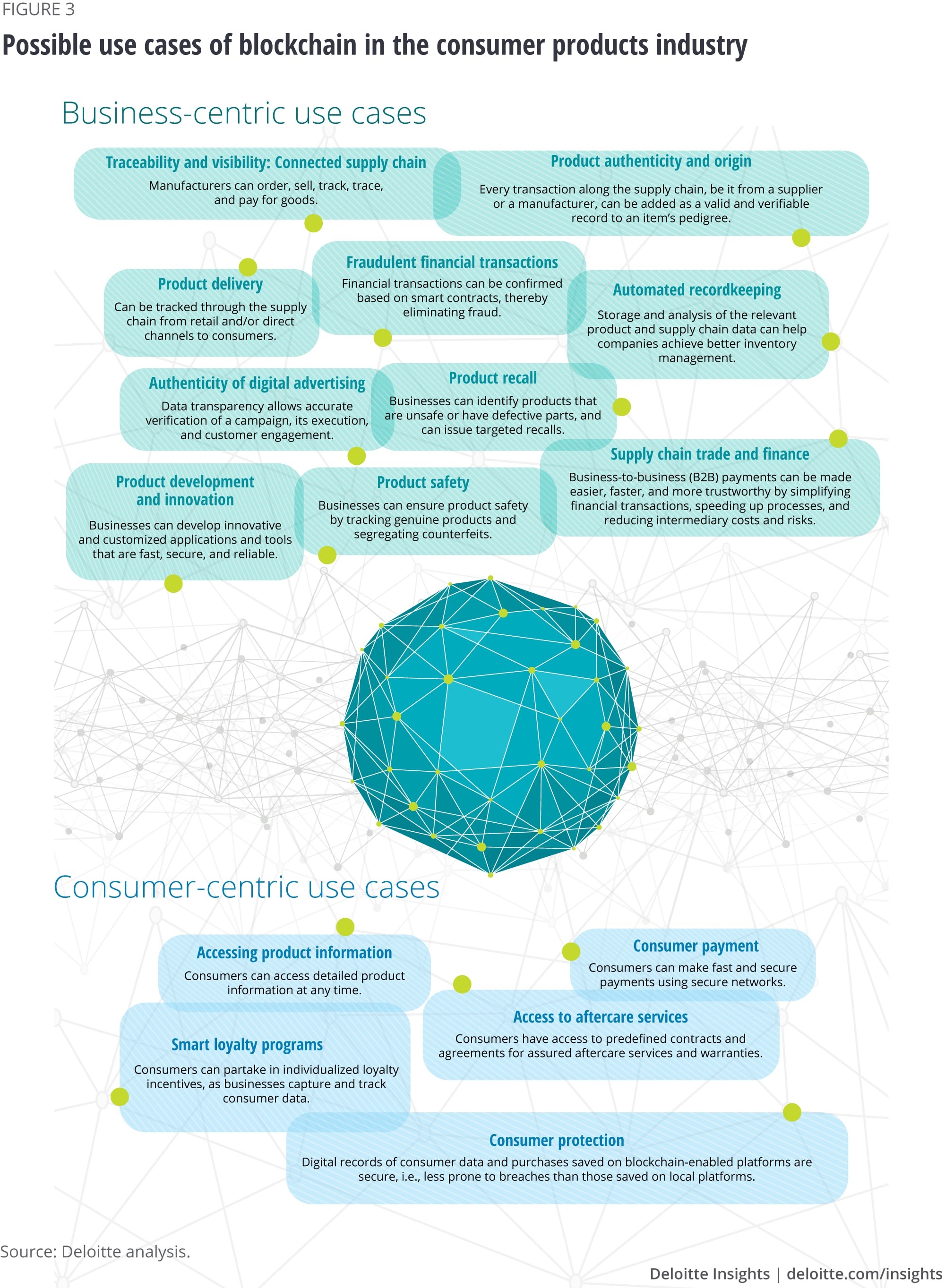

Blockchain has many potential use cases in the consumer products industry, especially with regard to tracking and monitoring of products and the flow of information, services, and money. Figure 3 represents a comprehensive collection of possible use cases. We have broadly categorized them as business and consumer centric, based on the beneficiary of the application.

Blockchain has many potential use cases in the consumer products industry, especially with regard to tracking and monitoring of products and the flow of information, services, and money. Figure 3 represents a comprehensive collection of possible use cases. We have broadly categorized them as business and consumer centric, based on the beneficiary of the application.

Consumer products companies would likely benefit from developing a perspective based on the use cases and case studies (see sidebar), identify the use cases with the greatest potential to positively impact their organizations, and then customize them based on their individual requirements. Further, identifying and allocating resources that include finance, talent, and infrastructure with a clear road map for implementation will likely contribute to the success of blockchain implementation. Global blockchain revenue may grow from approximately US$2.34 billion in 2017 to as much as US$13.9 billion by 2022, at a compound average growth rate of 42.8 percent.4 Nonetheless, companies may need to recognize that capital investments in blockchain can require a medium- to long-term time frame to realize a return on investment. It is especially true given the interplay of several factors, such as the lack of a supportive regulatory and legal framework, rapid changes in technology, talent gaps, and building a working consortium to operationalize blockchain.5

Case studies

Cargill completes a trade-finance deal using a single blockchain system

Facilitating B2B payments is an important use case of blockchain as the technology can simplify, secure, and expedite the payment process, while reducing intermediary costs and risks. In May 2018, Cargill and a top 10 global bank completed the world’s first commercial trade-finance transaction using a single, shared digital blockchain-enabled application, rather than multiple systems, which minimized the time taken to complete the transaction and the paper trail.6

Coca-Cola deploys blockchain to help mitigate the use of “forced” labor in the beverage industry

Food and beverage companies have been concerned about the issue of deploying “forced” labor in countries where this practice is commonplace. Coca-Cola has come under the spotlight for sourcing sugarcane from such countries. In March 2018, Coca-Cola and the US State Department announced that they are using blockchain’s digital ledger technology to create a secure registry for workers worldwide. The secure registry will help companies like Coca-Cola hire and deploy labor that has genuinely chosen to work, thus helping ensure complete transparency for fair and equitable wages.7

Show more

Being on the leading edge of disruptive technologies

Newer and bolder disruptive technologies are continuously transforming and changing the way companies conduct their business by driving operational efficiencies and enhancing the customer experience. Notably, disruptive technologies are exponential in nature—their applications can provide advantages that considerably boost the output and efficiencies of processes they impact, resulting in a multiplier effect. For example, almost all blockchain use cases involve the Internet of Things (IoT) at either the front or the back end of the application. During the 2017 US Thanksgiving season, when Cargill deployed blockchain technology to let consumers trace the source of their turkeys, it used IoT-based barcodes that could be scanned by smartphones.8

Blockchain is one example of a disruptive technology that can potentially help consumer product’s companies move along or even ahead of the digital transformation curve. Blockchain’s potential in the consumer products space is unlimited. Our article Adapting to landmark labeling laws in the food industry through blockchain and the internet of things9 demonstrates the practical applications of blockchain in the food industry for traceability, visibility, and recall as well as for accessing product information. Watch out for future articles in this series on disruptive technologies in the consumer products industry addressing AI, DR, and cloud.

Blockchain is one example of a disruptive technology that can potentially help consumer product’s companies move along or even ahead of the digital transformation curve. Blockchain’s potential in the consumer products space is unlimited. Our article Adapting to landmark labeling laws in the food industry through blockchain and the internet of things9 demonstrates the practical applications of blockchain in the food industry for traceability, visibility, and recall as well as for accessing product information. Watch out for future articles in this series on disruptive technologies in the consumer products industry addressing AI, DR, and cloud.